Regulatory Oversight of Fiduciary Services For Hire

Regulatory Oversight of Fiduciary Services For Hire

Regulatory Oversight of Fiduciary Services For Hire Read More »

Regulatory Oversight of Fiduciary Services For Hire

Regulatory Oversight of Fiduciary Services For Hire Read More »

South Dakota Division of Banking Updates & Emerging Issues

South Dakota Division of Banking Updates & Emerging Issues Read More »

The largest generational money transfer in history is already upon us. As baby boomers pass trillions of dollars to their Generation X and millennial offspring, how are you positioned to help your clients with a smooth transfer of that family wealth? And how is your practice equipped to retain the business of surviving spouses and younger generations when they inherit assets? Advisors like you play a crucial role in stewarding this money in motion. Full of examples, this presentation provides you and your business with a practical, step-by-step roadmap to assist clients in preserving their generational wealth.

Moderated by Patrick Goetzinger, members of the Task Force will discuss the work of the Task Force in shaping South Dakota trust law for the upcoming 2022 legislative session and review new trust laws that became effective in 2021. By Executive Proclamation, the Task Force’s goal is to establish and maintain South Dakota’s stature as the premier trust jurisdiction in the United States. The Task Force, the only one of its kind in the nation, is comprised of representatives from the trust industry, recognized as experts in their field, and ex-officio appointments from state government agencies. The panel is a cross section of the Task Force membership. A portion of the discussion will be dedicated to a Q&A session with attendees.

GOVERNOR’S TRUST TASK FORCE Read More »

This session’s topics will include: a primer on blockchain and digital assets, an overview of some innovative use cases for the financial services industry, a review of significant regulatory developments and how it may impact the industry, and a look towards the future under the Biden administration. No prior understanding of blockchain or digital assets is required, just a curiosity of what it all means.

JAMISON SITES & BENNETT MOORE Read More »

Director Afdahl will provide an update on trust company statistics and trends as well as developments related to national trust charters. Industry guidance will be covered to include existing guidance issued by the Division as well as potential areas for new guidance. A brief discussion of potential legislative items for the 2022 SD Legislative Session will be provided.

Your goal is to connect with and convert prospects to build life-long customers for your business. But most financial professionals don’t connect as they could because they lead with NUMBers when what their audience really wants is a story. Therefore, in the Business of Story Masterclass, you will learn the foundational narrative framework of the ABT (And, But, Therefore) that hooks the primal part of your customer’s brain where all of the real buying decisions are being made. The goal of the session is to help you become a more confident, clear and compelling communicator to ignite the growth of your business and career.

Directed trusts continue to grow in popularity. And with good reason. They allow a trust settlor to direct in advance the management of trust assets and beneficiaries. Many states, including South Dakota, have facilitated the growth of directed trusts with broad exoneration statutes. However, these statutes may have an inadvertent downside — complacency amongst directed trustees, seemingly secure that they are insulated from liability. Such complacency, of course, needs to be avoided. Indeed, what makes directed trusts so appealing also makes them ripe for potential litigation. For example, a unique or special asset like a family business may be particularly well suited for a directed trust. But these assets are trickier to manage than a basket of stocks and bonds. Similarly, beneficiaries requiring extra attention may also be appropriate for a directed trust but, again, this beneficiary raises the risk profile. In order to avoid liability, directed trustees, and the other fiduciaries that work with them, must be vigilant in adhering to direction and otherwise carefully carrying out their particular role. We will discuss how best to accomplish this with a goal we can all agree is a worthy one — litigation avoidance.

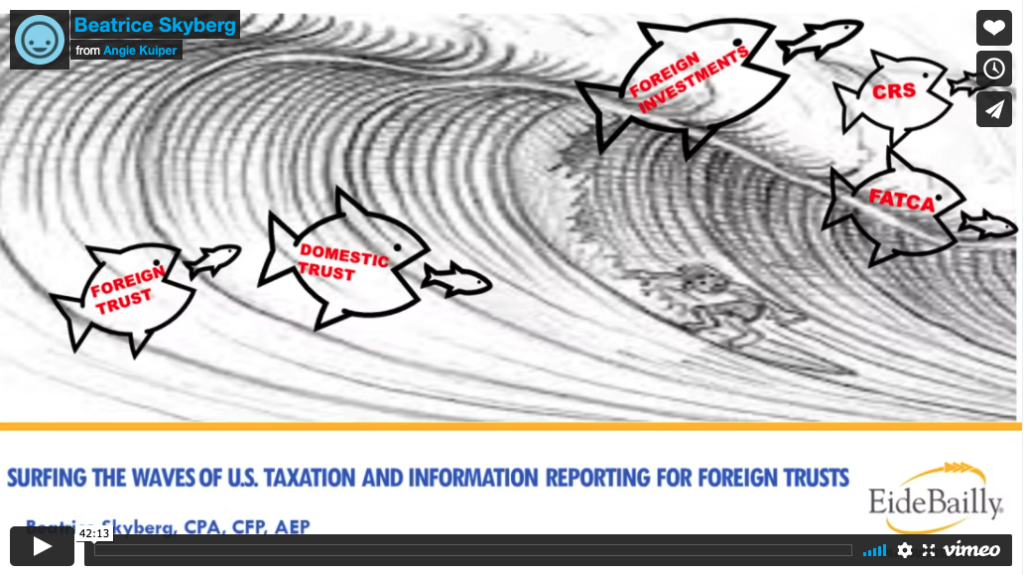

This presentation is intended to navigate the audience through the complexities of U.S. taxation and information reporting requirements for the foreign trust. It will also explain the compliance obligations related to the domestic trusts with foreign assets or foreign beneficiaries. Topics to be covered:

• Is it a foreign trust or domestic trust?

• If it is a domestic trust, are we off the hook from foreign reporting?

• If foreign trust, what’s next?

• What are the reporting obligations of trustee, grantor, beneficiary and underlying entities?

• Penalties and Possible Abatement

It seems that every day there is more bad news about the threats to organizations and their data, with no sign of hackers letting up any time soon. Despite this, there are many things that organizations can do to increase their security. In this presentation we will discuss the most common threats, how to understand the actual risk to your organization, and provide information on what can be done to become more secure.